What is the Regulations (REG) CPA Exam Section?

The Regulations (REG) CPA exam section tests candidates’ knowledge of federal taxation for individuals and companies of all kinds as well as business transaction law. REG is often considered difficult because it requires CPA candidates to understand complex tax laws and memorize key legal concepts.

The Regulations (REG) CPA exam section tests candidates’ knowledge of federal taxation for individuals and companies of all kinds as well as business transaction law. REG is often considered difficult because it requires CPA candidates to understand complex tax laws and memorize key legal concepts.

The REG exam section is the only part of the CPA exam that tests taxation and business law, so it doesn’t have much content overlap with any other sections of the CPA exam. Thus, some candidates without tax experience often struggle with REG. In order to be successful on the Regulations section, you will need to memorize tax formulas, figures, and legal case law.

Let’s explore the REG exam section and analyze the covered topics and concepts, how the exam is graded, and how to pass the REG exam.

How Long is the REG Exam Duration?

The REG exam is a four-hour long test with an optional 15-minute break after the multiple-choice testlets. The break time does not count towards the overall 4 hour time length. Thus, the total time with the optional break is 4 hours and 15 minutes.

There are no time limits for the individual MCQ and TBS testlets, so you will need to manage your time throughout the entire exam in order to finish it.

Likewise, there is no penalty for finishing the REG exam before the 4 hour time limit has expired, but it is a good idea to use the entire time to review tricky questions that you may need to look at a second time.

Finishing early also doesn’t add any additional points to your score, so it’s in your best interest take your time and review any questions you need to before the time is over.

REG Section Exam Topics & Materials Tested

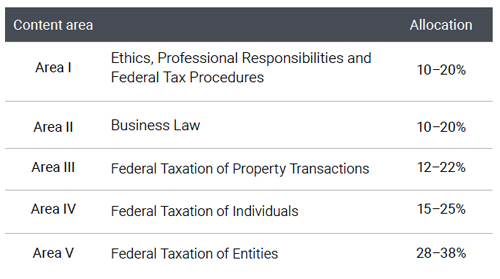

The REG exam section is designed to test your understanding of taxation a regulation law. There are 5 main content areas on the REG CPA exam including: Ethics, Professional Responsibilities, And Federal Tax Procedures; Business Law; and Federation Taxation For Property Transactions, Individuals, and Entities.

Below is a full list of the topics covered on the REG exam.

Ethics, Professional Responsibilities, And Federal Tax Procedures: It tests the candidate’s knowledge of the requirements set by the Treasury Department in Circular 230 relating to the rules to be followed by the tax-payers, the requirements of each of the US state boards concerning the CPA license, knowledge of federal tax procedures- necessary substantiation, disclosures, penalties, the hierarchy of authoritative bodies, and knowledge on legal issues affecting CPA practice.

Business Law: It covers knowledge of the accounting, financial reporting, and auditing aspects of business transactions, business contracts, government regulations relating to business, debtor-creditor relationships, and business structure, federal and state laws affecting business operations.

Federation Taxation For Individuals, Entities, And Property Transactions: The topics tested in this area include federal income tax rules, accounting methods, and gift and estate tax. Area 3 covers the topics specifically relating to taxation on property transactions, Area 4 covers individual tax preparation and tax planning.

Area 5 covers taxation of entities such as sole proprietorships, limited liability companies, partnerships, S corporations, C corporations, joint ventures, estates, trusts, tax-exempt organizations, again for tax preparation and tax planning knowledge.

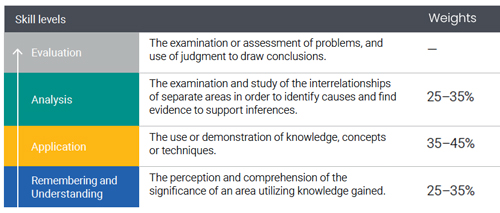

REG tests candidates on the content areas using an almost even distribution of analysis (25-35%), application (35%-45%), and memory/understanding (25%-35%) skills. REG does not focus on evaluation skills like AUD.

Regulations (REG) CPA Exam Structure & Format

The REG exam section consists of 76 multiple-choice questions and 8 task-based simulations. The test is divided into five testlets: 2 MCQ testlets with 38 questions in each testlet and 3 TBS testlets with 2 questions in the first testlet and 3 questions each in the other two testlets.

One thing to keep in mind is that not all of the multiple-choice questions are graded. Some of the questions are pre-test questions that the AICPA uses to test how candidates respond to their difficulty level for future exams. There is no way to identify between an operational and a pretested question.

Of the 76 MCQs on the REG exam, 12 questions are pretested while only 64 are counted towards the exam score. Of the 8 Task-based simulations, 1 is pretested and 7 are operational. This means that these questions will not affect your score whether you answer correctly or not.

The REG exam starts with the two MCQ testlets. After you complete both of these sections, you will be allowed to take a 15 minute break before you jump into the simulations testlets.

Here’s a chart of the REG exam question format and structure of multiple-choice questions (MCQs) and test-based simulations.

REG Section Exam Structure

| REG CPA Exam Section | 2022 CPA Exam | 2021 CPA Exam |

|---|---|---|

| Multiple-choice Questions | 76 | 76 |

| Task-based Simulations | 8 | 8 |

| Written Communications | 0 | 0 |

REG Section Exam Format

| REG Exam Testlets | Question Types | Time / Duration |

|---|---|---|

| Testlet #1 | 38 Multiple-choice Questions | 60 minutes |

| Testlet #2 | 38 Multiple-choice Questions | 60 minutes |

| Testlet #3 | 2 Task-based Simulations | 30 minutes |

| Testlet #4 | 3 Task-based Simulations | 45 minutes |

| Testlet #5 | 3 Task-based Simulations | 45 minutes |

REG CPA exam Study Tip: Multiple-choice questions rarely list answers that are all equally likely. If you get stumped on a question, use process of elimination to reduce the number of possible correct answers. More likely than not, you will be able to immediately remove two answers and be left with a 50/50 chance of picking the correct answer.

Multiple Choice Questions

The 72 multiple-choice questions on the REG exam are broken into two 36 question testlets. The first testlet will include medium difficult questions. If you score well on these questions, the exam will generate a more difficult set of questions for your second testlet.

This is a good thing because harder questions are worth more on the exam. If you answer a more difficult question correctly, it will add more points to your score than if you answer multiple easy questions correctly.

If you score poorly on the first testlet, you will get an easier second set of multiple-choice questions. Keep in mind, 12 questions are pre-test questions that are not graded.

Overall the MCQs account for 50% of your REG CPA exam score.

REG CPA exam Study Tip: Memorize all of the basic tax fact and figures. Make a cheat sheet to memorize every important tax number like standard deductions, rates, and exemption amounts. You don’t want to second guess yourself on the exam, so it’s best to memorize as many easy facts as you can.

Task-Based Simulations

The 8 REG task-based simulations are split between research, taxation calculations, and legal concept applications. Unlike the tax problems that appear in the MCQ sections, the TBS questions do not give you answers to choose from. You will be required to calculate the answer and fill in the blank text field. This is much harder.

The REG exam simulations are designed to test your overall understanding of tax and legal concepts as well as you ability to apply the concepts. Thus, the questions may require you to compute multiple parts of a tax return in order to get to the final answer.

Like the MCQ sections, there is one pretest simulation that you will be unaware of. This question will not count toward your final score in any way.

REG Exam Testlet & Simulation Time Length/Duration

The REG exam section is a four hour long test that is divided into 5 different testlets. Each testlet is not individually timed and does not have time limit, so you it’s up to you to manage your time well enough to complete the exam without running out of time.

How to manage your REG test time

The most important thing you can do on the REG section is budget your time. Spending too much time on a single section or question will come back to bite you in the end. You will most likely run out of time and your score will suffer for it.

This is particularly true when it comes to the MCQs. If you spend too much time on the MCQ testlets, you won’t leave yourself enough time to finish the TBS. Remember the TBS accounts for 50% of your score. You need to finish this section.

The best way to manage your time on REG is to split the exam into sections. Spend no more than 60 minutes on each MCQ testlet. This will give you 45 minutes to answer the questions and 15 minutes to go back and review any questions you marked for follow up. This will give you 2 hours to finish the TBS or 15 minutes for each simulation.

Give yourself enough time to finish the simulations. The tax and legal sims can be tricky because they often involve a lengthy explanation to setup the question.

Keep your eye on the clock while you are navigating the exam. If you pay attention to the time, you shouldn’t have a problem finished the exam.

How Is REG Graded & Weighted?

The REG section weights both the MCQs and task-based simulations equally at 50% of your score. This is why it’s so important to leave yourself enough time to finish the simulations. It doesn’t matter how well you do on the multiple-choice questions, it won’t be enough to pass the exam without simulations.

REG has an extreme emphasis on taxation. This subject is so broad it consumes about 75% of the entire REG exam.

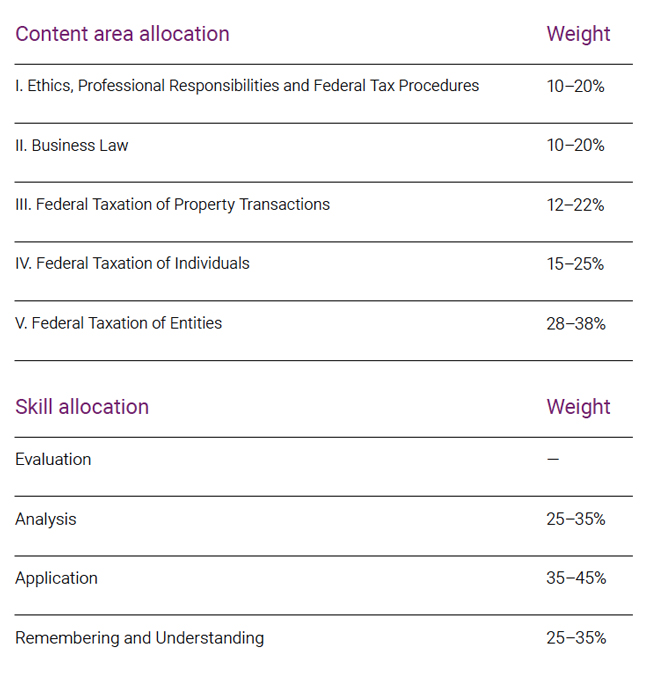

Below is the AICPA content area and skill allocations for the REG exam section along with the graded weights of each. This AICPA report shows how the REG exam is distributed and what knowledge and skills are tested in each content area.

The REG exam content is weighted in the following ratios: 55-85% of questions test the candidate’s knowledge of Federal Taxation, 10-20% of each question are related to Business Law and Ethics, Professional Responsibilities, and Federal Tax procedures.

The candidate is tested against the skill levels relating to the topics mentioned above, with 25-35% weightage each given to remembering and understanding and Analysis skills, and 35%- 45% weightage is given to the Application aspect.

MCQ & Simulation Grading Percentage Distributions

The REG exam section multiple-choice questions and task based simulations are graded equally. This means that each section accounts for half of your overall score. This wasn’t always the case as MCQs had more scoring significance in prior years’ exams.

This also means that you must do well in both sections. It will be difficult to pass REG by doing well in one section and poorly in the next. You will need to work on both multiple-choice questions and simulations in order to pass REG.

50% of your REG score consists of your performance on the 72 multiple choice questions, while the other 50% of your score relies on your performance on the 8 simulations.

| CPA Exam Section | Grading Score Distribution |

|---|---|

| AUD | MCQs: 50% TBSs: 50% |

| BEC | MCQs: 50% TBSs: 35% WC: 15% |

| FAR | MCQs: 50% TBSs: 50% |

| REG | MCQs: 50% TBSs: 50% |

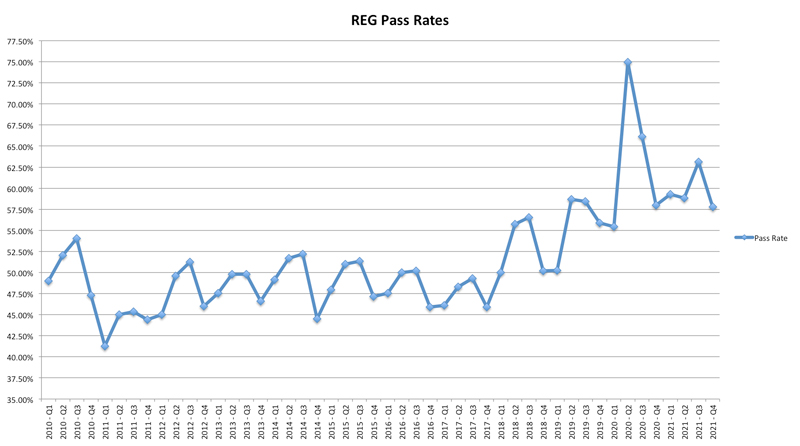

REG Exam Pass Rates

Here is a graph of the REG CPA exam pass rates from 2010 to the present:

The REG exam pass rates have consistently increased for the past ten years. Unlike some of the other CPA exam sections, REG saw a spike in 2020 CPA exam scores that didn’t drop significantly under prior year pass rates.

It’s quite the opposite. REG pass rates saw a sharp increase in 2020 and continued the multi-year increasing trend after the lockdowns ended. This increase seems to coincide with the scoring change when the AICPA increased the emphasis on simulations and decreased the focus on multiple-choice questions.

Either way, the REG CPA exam pass rates have continued to climb showing that it is the second easiest CPA exam section right behind the BEC section. This might change when the AICPA implements the new CPA evolution framework later in 2024. You can find more information about that on the AICPA website.

Regulations (REG) CPA Exam Study Tips

On average, CPA candidates need to study between 84 and 112 hours studying for the REG section of the exam. This is obviously different for every candidate and largely depends on your knowledge and experience with federal taxation. Here are a few study tips that you can implement into your study sessions to reduce your study time and help ensure you pass REG on your first try.

Memorize Facts: One of the most important ways to prepare for REG is to memorize all of the key tax facts like exemption amounts, deduction limits, and loss carry forwards/backs. The questions are written to trip you up on these simple topics, so do yourself a favor and memorize them.

Experience Matters: You will be miles ahead on the REG section if you have professional tax experience. You will most likely already have many of the tax numbers and formulas memorized, but you might need to work on the business law problems. Know your experience and what you need to study more.

Practice Problems: There is no substitute for practicing REG tax problems. Many of the problems that appear on the exam involve calculating multiple steps to arrive at an outcome. You need to practice doing these types of problems, so you won’t get stumped on the exam.

Testing Time: Take REG when you have time to prepare for it. Many tax professionals think they can take it right after tax season because all of the information is fresh in their mind, but it’s not the case. You need to actively study for REG. If you don’t, you will likely fail.

Should I take the REG exam first?

REG is a great first CPA exam section for tax professionals who have a good amount of experience working in taxation or recent college graduates who have an excellent grasp on taxation and law concepts. It seems like tax just clicks with some students while others have a hard time with it. If you are a tax person, you will know it.

The most important thing is that you take the CPA exam you are most comfortable with first. Your strongest CPA exam section should the first one you take because it gives you a leg up on your first exam and if you need to retake it because of the 18-month window, you will have no problem passing it again.

Should I take the REG exam last?

The REG CPA exam is a good last section for candidates who struggle with taxation and business law concepts. If you were bored to death in your tax classes in college, you will most likely want to take the REG section last because it’s your weakest subject.

You should always aim to take your weakest CPA exam section last because it gives you the most time to prepare for it. In the unlikely event that you fail it, you will be able to focus on REG without thinking about taking any other exam in the future. It’s the last hurdle.

If you struggle with tax and law concepts, you should take the REG CPA exam section last.

Who Is the REG Exam Easiest For?

Regulations has one of the highest pass rates out of any CPA exam section with more than 57% of candidates passing it in the last testing window. The REG exam is often easiest for professionals with taxation experience and new graduates who did well in their taxation and business law classes.

Here are a few different CPA candidates who passed REG with ease:

Recent Taxation Students: People who have had Auditing and US tax-related subjects in their curriculum find it easier to perform in REG.

Tax Professionals: People with professional experience in the external or internal audit field or people who have worked under CPAs and have done Internal Revenue Service Audits can understand the concepts of the test well.

Other Accounting Professionals: Also, candidates who have recently completed any of the financial certifications like Chartered Certified Accountant (ACCA), Certified Financial Planner (CFP), Certified Management Accountant (CMA), or Chartered Alternative Investment Analyst (CAIA) might have the concepts fresh in their mind which they can use on the Regulations section.

Who Is the REG Exam Hardest For?

Although the Regulations CPA exam section has one of the highest pass rates, plenty of CPA candidates struggle with this test. Passing REG involves memorizing numerous complex tax codes and business law cases.

Not everyone is cut out for tax and legal work. The REG CPA exam section is hardest for candidates with little experience in taxation and difficulties memorizing numerous facts and cases verbatim. Here are some examples of CPA candidates who struggle with REG.

Inexperienced Candidates: People with absolutely no tax background find it harder to take the REG exam. Since the exam requires practical application of concepts, knowing the tax laws is not enough. The candidates need to have a high-level understanding to be able to solve practical problems, particularly in task-based simulations.

Poor Preparation: Preparing for REG takes time if you are an inexperienced candidate. You need to take the time to make flashcards and any other study aid that will help you memorize all of the key facts that you need to recall on the exam. Make studying a priority and you should do fine on REG.

Auditing Students: Many CPA candidates who do well in auditing do poorly on REG. These two subjects seem to be opposite one another. Chances are if you enjoy taxation, you probably hate auditing and the same is true from the other perspective. If you are an auditing student, you may need to spend some extra time studying for REG.

Other CPA Exam Sections

- AUD CPA exam section

- BEC CPA exam section

- FAR CPA exam section

- REG CPA exam section

- Breakdown of all 4 CPA exam parts

What’s the best CPA study course for REG?

The only way to pass the Regulations section of the CPA exam is study with a proper review guide. There is no way to memorize all of the facts and topics that you need to know without a full length review course, so which should you get?

The best CPA exam study book for the REG section depends on the way you learn. Some CPA candidates are visual learners and have the easiest time learning from video lectures or instructors explaining topics to them while other candidates prefer to work problems and don’t get much out of watching videos.

The right course for you might be different than the right course for another candidate. It’s important to match your learning style with the course that is best suited for that. The best REG CPA course is the one that works best for you.

We’ve reviewed all of the top CPA courses and give detailed explanations of their teachings styles, so you can pick out the one that will help you pass REG the fastest.