Every year the AICPA changes different aspects of the CPA exam. These changes are published in their annual CPA exam blueprint.

Every year the AICPA changes different aspects of the CPA exam. These changes are published in their annual CPA exam blueprint.

In 2023, the AICPA published its new 2024 blueprints for the CPA exam that change it drastically from prior years’ examinations.

The new format changes not only the structure and scoring of the exam but it also changes the testing windows and exam dates available for candidates.

Let’s walk through the latest AICPA CPA exam changes, so you can better understand the exam and how to pass it in the coming year.

What is the AICPA CPA Exam Blueprints?

The CPA exam blueprints is the framework and format CPA exam changes for the upcoming CPA exam published by the AICPA each year.

The AICPA created the CPA exam blueprints to help CPA exam candidates understand the content topics and skills tested in the uniform CPA exam.

The CPA Examination Blueprints are intended to help you prepare for the CPA test while also considering the minimum skills and knowledge level required for immediate licensure once you become a CPA. While it is beneficial to consult the blueprints for a better understanding of what is expected of a CPA, you do not need to be concerned about them.

Here is a guide we’ve created to help you with the course material using the blueprints to help you prepare for the CPA exam.

What are the 2023-2024 CPA Exam Changes?

On October 23, 2020, the Board of examiners approved the Practice Analysis a Final Report and July 1, 2021 Blueprints, effective July 1, 2021. In 2024, the AICPA will officially move to the CPA Evolution CPA exam format that focuses on core plus discipline model.

The changes are now available, and the various blueprint revisions have been reduced to the most crucial takeaways by test. Some content has been removed, with some added, and topics have been deemphasized with the skills level required to be demonstrated reduced. Here are the changes.

The 2021 CPA exam changes mainly covered BEC and AUD and were established due to the need for candidates to be familiar with data analytics and have a data-driven mindset, understand business processes and IT enabling them plus related controls and risks, and organization and system controls for service organization.

In BEC, the items will be assessed from a management’s perspective, while in AUD, the evaluation will be from the auditor’s view. Interestingly, REG and FAR don’t have any additional content, but they have been reduced.

AUD Exam Blueprint Changes

The CPA exam’s Auditing and Attestation Section tests basic skills and knowledge that a newly certified CPA should show when conducting audit, attestation, and accounting review engagements.

As a licensed CPA, you should demonstrate skills and knowledge related to your professional duties, including independence, ethic, and professional skepticism.

Also, you should understand an entity, including its information system, operations, and underlying business processes, plus transactions flow and underlying data.

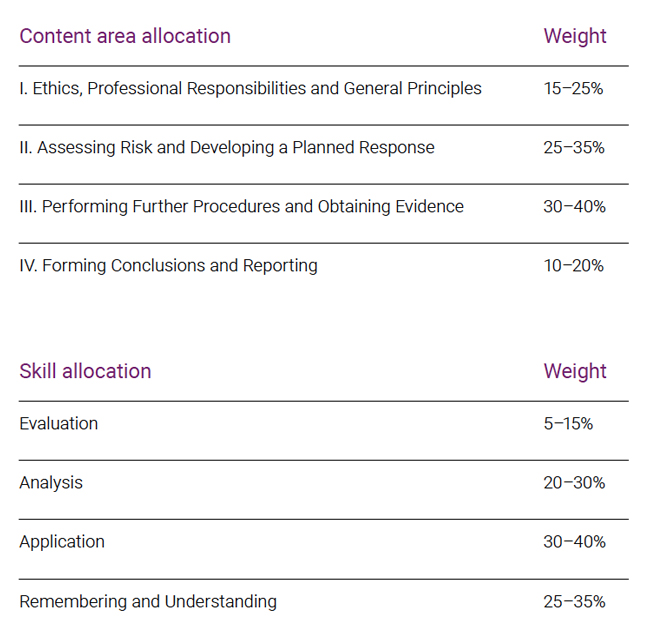

Content Allocation

Content in the AUD blueprint is categorized by AREA, GROUP, and TOPIC. Every topic comprises one or more TASKs that you will be required to do during attestation, audit, and accounting and review service engagements.

It is vital to note that the engagements evaluated under AUD are as per professional standards and regulations set by various bodies. The tasks that are part of AUD do relate to different engagements and can be applied in audit, attention, and accounting, and review service engagements.

Content areas are grouped into four areas:

Skill Allocation

The AUD Examination tests high order skills and based on the task’s nature, every representative task in the blueprint is given a skill level. The first skill is Remembering and Understanding, which is concentrated in Areas I and IV. Tasks relate to perception and understanding of knowledge gained.

The other skill level is application, which is tested in all areas of AUD with a focus on topics like documentation and professional responsibilities. Analysis and Evaluation skill levels are evaluated in Area II and III, covering tasks like concluding insufficiency and appropriateness of evidence.

Composition

You should be aware of engagement type and entity type in the question when answering multiple-choice questions, research prompts, and task-based simulations. You have four hours to complete the AUD exam. The AUD section comprises the Pre-Exam, Exam, and Post exam parts.

The exam has 72 multiple choice questions and eight task-based simulations. The pre-exam takes 10 minutes before starting the exam, and you will sit the exam for four hours with a 15-minute break between then MCQs and task-based simulations.

Score Weighting

Scoring in AUD, you need to score a 75 or more to pass, and 50% of the score will be derived from multiple-choice questions and the other 50% from the task-based simulations. You should be aware that there will be no penalty for a wrong answer, and the correct answer gains points while a wrong or no answer gets zero points.

At first, you will begin with a medium-difficulty multiple-choice testlet, and if you do well in this testlet, the next will be more difficult. It is important to note that you will gain more points attempting more difficult questions. For task-based simulation questions, they will not change based on performance, but you may receive credit for non-research-based simulation questions if part of the answer is correct.

BEC Exam Blueprint Changes

BEC, which stands for Business Environment and Concepts, is a section of the CPA exam that tests the role of a CPA in the business environment, covering topics that relate to various business areas like operations and corporate governance.

It is vital to note that CPAs should understand the business environment regardless of whether you want to be in a public accounting firm or internally within a company.

To assist you in getting familiar with the BEC CPA blueprint, here is a guide that will help you understand the content covered section format, skill levels, and how it is scored.

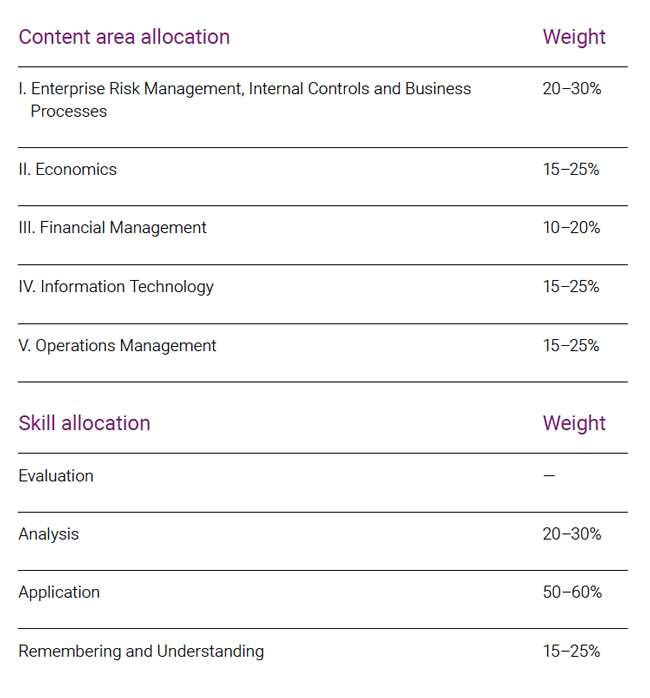

Content Allocation

There are five content areas of the BEC exam are as follows:

Skill Allocation

Different skill levels are tested, and each has a different exam content allocation.

Level I is remembering and understanding, which covers 15-25% of the exam.

Level II is the application that covers 50-60% of the exam.

Level III, which is the analysis covering 20-30% of the exam allocation. You will face more of the application and analysis in the written communication and task-based simulation areas of the BEC.

Composition

There are 62 multiple choice questions in the BEC exam and four task-based simulations, and three written communication tasks. Out of the 62 MCQs in BEC, around 12 will be pretest questions that don’t count towards your test score.

Task-based simulations require you to type your answers and may entail journal articles, research questions, cost accounting, and ratio calculations. There are four task-based simulations, and one will be a pretest not counting to your score.

Written communication tests your ability to communicate, and you are informed of a memo directed at a given audience. Out of the three tasks, one will be a pretest task.

The BEC exam is four hours long, and you will have a 15-minute break between the first and second task-based simulation tests. Also, there are optional breaks after the first MCQ testlets and the second testlet, but during this time, the timer will continue running. You need to keep track of time regarding the number of questions completed and how many you need to complete.

Score Weighting

Around 50% of your score will be from MCQs, 35% will be from task-based simulation, and 15% will be from written communication. Remember that in this exam, you equally have to score 75 for you to pass. You will be presented with medium-difficulty MCQs at first, and if you do well, the next testlet will be more difficult.

The more difficult questions will be worth more than the medium questions. For task-based simulations and written communication, the questions will not change relative to your performance.

FAR Exam Blueprint Changes

FAR stands for Financial Accounting and Reporting, which is a part of the CPA exam assessing skills and knowledge that newly licensed CPAs should show in financial accounting and reporting frameworks.

The section is the most comprehensive CPA exam that is often considered the most difficult. It covers various topics ranging from depreciation calculation where financial statements that are needed for governmental institutions.

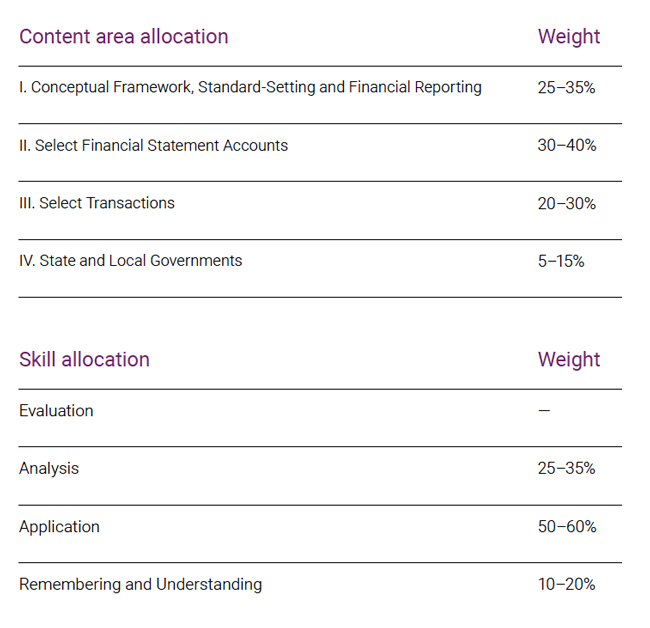

Content Allocation

There are four content areas in FAR:

Skill Allocation

The skills levels tested include remembering and understanding, which covers 10-20% of the exam. Level II is application which covers 50-60% of the exam, and level III is analysis which covers 25-35% of the exam.

Besides having a strong understating of some concepts, you also need to know how to apply them in certain situations. There are more analysis and application questions in the task-based simulation part.

Composition

There are 66 multiple choice questions in FAR, and out of these, 12 will be pretest questions that are not counting to your score.

You will also encounter eight task-based simulations, which are practical questions that require you to type your answers and may include filling out financial statements, research questions, filling a form with several questions, or journal entries. Out of the eight task-based simulations, one will be a pretest question that doesn’t count towards your score.

The exam takes four hours with a 15-minute break between the first and second task-based simulations tests. You will also be entitled to two optional breaks after the first MCQ and second MCQ test, but during these breaks, the timer will not stop.

Score Weighting

The MCQ and task-based simulation sections will each account for 50% of the score, and you need to score 75% to pass. There is no penalty for a wrong answer, and if you give a wrong answer or no answer, you won’t get any point, but a correct answer gains you a point.

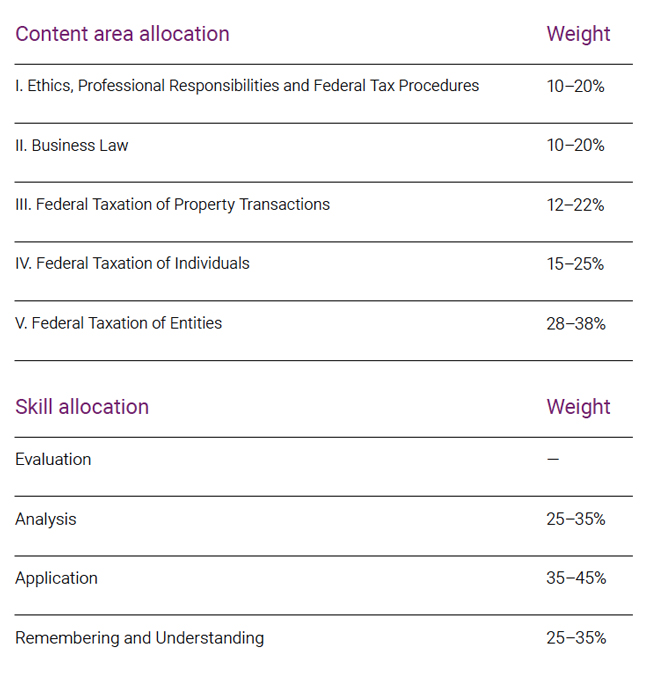

REG Exam Blueprint Changes

REG (Regulation) is part of the CPA exam that tests skills and knowledge of business law, federal taxation and ethics, and professional roles associated with tax practice.

Although the topics are similar, the extent of each topic appears to be expansive. You should have a firm grasp of tax concepts and how you can use them in business law to pass the exam.

Content Allocation

REG has four parts covering the tax side of the profession. Here are the areas and the percentage allocation in the exam:

Skill Allocation

Skill levels tested include remembering and understanding accounting for 25-35% of the exam, while application and analysis, which are tested in Area III, IV, and V, account for 35-45% and 25-35%, respectively.

Composition

There are 76 multiple choice questions in REG, and eight task-based questions. MCQs are one sentence or paragraph-long question that potentially has four answers. Out of the 76 MCQs, there are 12 pretest questions not counting towards your score.

On the other hand, task-based simulations are practical questions that will require you to type answers. Out of the eight task-based simulation questions, one will be a pretest question.

The exam also takes four hours with 15 minutes break between the first task-based simulation and the second task-based simulation. You can take two optional breaks, but during that time, the clock doesn’t stop.

Score Weighting

The passing score is 75, and the MCQs and task-based simulations will account for 50% of the score each. Equally, in this section, there is no penalty for a wrong answer, and each correct answer will gain you points, but a wrong answer or no answer means you get zero points.

How can you use the AICPA blueprint to pass the CPA exam?

The blueprint has been created to document the minimum skills and knowledge level that is required for you to receive a CPA license.

It is important in helping you prepare for the CPA exam by outlining what is required of you in terms of the contents covered topics are the scoring system.

By understating these, you will be better prepared for the exam.